Asuransi Jiwa Seumur Hidup:Apakah Ini Investasi Cerdas? Memahami Fakta

Terdapat lebih dari 400.000 agen asuransi di negara ini, dan hampir semuanya dengan senang hati menjual polis asuransi jiwa kepada Anda. Jika Anda membeli polis dengan premi $40.000 per tahun, komisi biasanya berkisar antara $20.000 dan $44.000 untuk agen tersebut. Seperti yang Anda bayangkan, komisi tersebut bisa sangat memotivasi, terutama mengingat pendapatan rata-rata agen asuransi sebesar $49,840. Lebih buruk lagi, banyak kebijakan terburuk yang menawarkan komisi tertinggi. Sayangnya, sebagian besar polis yang dijual dijual secara tidak tepat dan sebagian besar yang menjualnya adalah penjual yang menyamar sebagai penasihat keuangan.

Sebagai akibat dari konflik kepentingan yang menggelikan ini, para agen sering kali membuang beberapa mitos serius dalam upaya membujuk Anda untuk membeli produk mereka, yang mungkin menjelaskan statistik yang memberatkan bahwa 80%+ dari mereka yang membeli produk ini membuangnya sebelum kematian dan jajak pendapat dari dokter di dunia nyata di situs ini dan grup Facebook kami menunjukkan bahwa sebagian besar dari mereka yang telah membeli polis seumur hidup menyesali pembelian mereka. Jika ini semua adalah berita baru bagi Anda, bacalah Semua yang Perlu Anda Ketahui Tentang Asuransi Jiwa Seumur Hidup sebelum melanjutkan postingan ini.

Meskipun sebagian besar anggota grup FB WCI belum pernah membeli asuransi jiwa seumur hidup, 76% dari mereka yang pernah membeli asuransi menyesalinya.

Memuat ...

Jumlahnya serupa tetapi sedikit lebih rendah dalam jajak pendapat yang sedang berlangsung di situs ini (yang tidak seperti grup FB, mengizinkan pemungutan suara dilakukan oleh mereka yang menjual kebijakan ini).

Banyak orang mengira saya benci asuransi seumur hidup. Sebenarnya tidak. Saya benci cara penjualannya dan mereka yang menjualnya secara tidak pantas. Jika Anda sudah benar-benar memahami cara kerjanya dan masih menginginkannya, maka silakan membeli sebanyak yang Anda suka. Itu benar-benar tidak mempengaruhi saya. Tapi saya muak bertemu dengan pembaca dan pendengar yang TIDAK memahami cara kerjanya ketika mereka membelinya, dan begitu mereka memahaminya, TIDAK menginginkannya.

Cara Kerja Asuransi Jiwa Seumur Hidup

Asuransi Jiwa Seumur Hidup dapat diatur dengan berbagai cara, namun secara umum, Anda membayar premi bulanan atau tahunan untuk jangka waktu tertentu, atau sampai Anda meninggal. Semakin lama jangka waktu pembayaran premi, semakin rendah preminya. Setiap kali Anda meninggal, ahli waris Anda mendapatkan hasil dari polis tersebut. Karena setiap polis seumur hidup dijamin akan terbayar jika Anda menyimpannya sampai meninggal, preminya jauh lebih tinggi dibandingkan polis asuransi jiwa berjangka yang sebanding.

Polis asuransi jiwa seumur hidup, seperti jenis asuransi jiwa permanen lainnya, sebenarnya merupakan gabungan antara asuransi dan investasi. Polis ini mengakumulasi nilai tunai seiring berjalannya waktu. Nilai tunai tersebut tumbuh dengan cara yang dilindungi pajak, dan Anda bahkan dapat meminjam uang di sana bebas pajak (tetapi tidak bebas bunga). Setelah Anda meninggal, berapa pun yang Anda pinjam (ditambah bunganya) diambil dari tunjangan kematian, dan sisanya dibayarkan kepada ahli waris Anda. (Anda mendapatkan nilai tunai atau manfaat kematian, bukan keduanya.)

Aspek investasi ini memungkinkan mereka yang menjual asuransi seumur hidup menemukan segala macam alasan kreatif Anda harus membelinya dan cara kreatif untuk menyusunnya. Pendukung yang paling ekstrim bahkan mungkin berpendapat bahwa Anda tidak memerlukan produk keuangan apa pun sepanjang hidup Anda karena asuransi seumur hidup tampaknya dapat memenuhi semua kebutuhan Anda termasuk hipotek, pinjaman konsumen, asuransi, investasi, tabungan kuliah, dan pensiun.

Masalahnya adalah untuk setiap penggunaan asuransi seumur hidup, biasanya ada cara yang lebih baik untuk mengatasi masalah keuangan tersebut. Postingan ini adalah 38 mitos umum tentang asuransi seumur hidup yang disebarkan oleh para pendukungnya.

Mitos #1 — Seumur Hidup Bermanfaat untuk Perlindungan Pendapatan Pra-Pensiun

Asuransi jiwa seumur hidup bukanlah cara terbaik untuk melindungi penghasilan Anda, melainkan asuransi jiwa berjangka. Sebelum Anda pensiun, Anda dapat membeli asuransi jiwa berjangka yang murah untuk merawat orang yang Anda cintai jika Anda meninggal dunia sebelum waktunya. Polis asuransi jiwa berjangka tingkat premium 30 tahun dengan nilai nominal $1 Juta yang dibeli pada usia 30 tahun yang sehat menghasilkan $680 per tahun. Polis seumur hidup serupa akan menelan biaya 10 kali lipat, $8,000-$10,000 per tahun. Yaitu uang yang tidak dapat digunakan untuk pembayaran hipotek atau liburan, atau diinvestasikan untuk masa pensiun.

Mitos #2 — Seumur Hidup Adalah Cara Terbaik untuk Mendapatkan Manfaat Kematian Permanen

Seumur hidup bukanlah cara terbaik untuk mendapatkan manfaat kematian permanen—kehidupan universal yang dijamin tidak akan berakhir adalah cara terbaik. Ada beberapa orang yang membutuhkan atau menginginkan polis asuransi yang akan dibayarkan pada saat kematiannya, kapan pun itu terjadi. Hal ini dapat berguna untuk beberapa masalah perencanaan perumahan yang tidak biasa. Namun, ada produk yang lebih baik yang menyediakan hal ini dan jauh lebih murah dibandingkan asuransi jiwa seumur hidup. Ini disebut Asuransi Jiwa Universal Tanpa Selang yang Dijamin . Ini TIDAK mengumpulkan nilai tunai apa pun tetapi hanya memberikan manfaat kematian seumur hidup. Biayanya hanya setengah dari harga asuransi jiwa seumur hidup, jadi Anda tidak akan terkejut mengetahui bahwa komisi agen atas penjualan ini akan jauh lebih rendah.

Sebut saja saya sinis, tapi saya kira itu mungkin salah satu alasan mengapa Anda belum pernah mendengar tentang jaminan kehidupan universal yang tiada batasnya. Asuransi jiwa seumur hidup memberikan jaminan manfaat kematian yang DIPROYEKSI (tetapi tidak dijamin) tumbuh perlahan sehingga jika Anda meninggal pada usia harapan hidup atau lebih lambat, Anda akan meninggalkan sedikit lebih banyak daripada manfaat kematian polis awal.

Manfaat Kematian dan Inflasi

Polis seumur hidup yang saya lihat baru-baru ini memproyeksikan manfaat kematian dari polis $1 Juta, yang dibeli pada usia 30 tahun, akan menjadi $3,17 Juta pada saat kematian pada usia 83 tahun. Kedengarannya bagus, hampir seperti perlindungan inflasi dari tunjangan kematian. Kecuali inflasi historis sekitar 3,1%. Pada tingkat 3,1%, $1 Juta sekarang akan setara dengan $5,04 Juta dalam 53 tahun. Kebijakan seumur hidup akan hancur karena inflasi yang tidak terduga, karena dividen terutama didukung oleh obligasi nominal, yang nilainya akan mati jika terjadi inflasi yang tinggi.

Oleh karena itu, asuransi seumur hidup bukanlah cara terbaik untuk memberikan jaminan manfaat kematian nominal seumur hidup atau jaminan manfaat kematian nyata seumur hidup. Jadi apa gunanya? Bagaimana dengan jaminan manfaat kematian yang mungkin meningkat jika perusahaan asuransi ingin meningkatkannya? Apakah Anda bersedia membayar premi dua kali lebih tinggi untuk itu? Menurutku tidak.

Mitos #3 — Asuransi Jiwa Seumur Hidup Memberikan Pengembalian Investasi yang Besar

Seumur hidup bukanlah cara terbaik untuk berinvestasi—investasi tradisional adalah cara terbaik. Ketika Anda membayar premi seumur hidup, sebagian dari uang tersebut digunakan untuk membeli asuransi, sebagian lagi digunakan untuk biaya overhead dan keuntungan bagi perusahaan asuransi, dan sebagian lagi digunakan untuk komisi penjual. Sisanya kemudian masuk ke bagian nilai tunai polis.

Setiap tahun, perusahaan asuransi mengumumkan dividen, dan jika ada $10.000 dalam porsi nilai tunai dan dividennya 6%, maka $600 akan dikreditkan ke nilai tunai Anda. Dividen hanya diterapkan pada nilai tunai, bukan seluruh premi yang dibayarkan, sehingga tingkat dividen rata-rata tidak ada hubungannya dengan pengembalian aktual Anda atas polis sebagai investasi. Faktanya, laba atas investasi umumnya negatif setidaknya selama satu dekade. Saya baru-baru ini menganalisis kebijakan untuk laki-laki sehat berusia 30 tahun dengan harapan hidup 53 tahun. Jaminan pengembalian nilai tunai kurang dari 2% per tahun SETELAH 5 DEKADE .

Bahkan jika Anda menggunakan nilai “proyeksi” optimis dari perusahaan asuransi, Anda masih melihat keuntungan kurang dari 5%. Pada kenyataannya, Anda mungkin akan mendapatkan keuntungan sebesar 3%-4%. Mengingat Anda harus mempertahankan “investasi” ini selama 5 dekade, sepertinya kompensasinya tidak seberapa. Jika Anda memiliki waktu puluhan tahun untuk berinvestasi, jauh lebih bijaksana jika Anda mengambil lebih banyak risiko dalam investasi Anda dan mendapatkan keuntungan yang lebih tinggi. Investasi pada saham atau real estat kemungkinan besar akan memberikan keuntungan selama beberapa dekade pada kisaran 7%-12%. $100.000 yang diinvestasikan selama 50 tahun dengan bunga 3% per tahun akan tumbuh menjadi $438.000. Jika pertumbuhannya sebesar 9%, Anda akan mendapatkan $7,4 Juta, atau uang 17 kali lebih banyak. Tingkat bunga yang Anda kumpulkan untuk investasi jangka panjang sangatlah penting, terutama dalam jangka waktu yang lama.

Mitos #4 — Perusahaan Asuransi Adalah Investor Hebat

Beberapa agen percaya bahwa perusahaan asuransi bisa mendapatkan keuntungan investasi yang tidak dapat Anda atau saya temukan di tempat lain dan meneruskan keuntungan besar tersebut kepada pemilik polis mereka. Melihat ke balik terpal dan melihat apa yang sebenarnya ada dalam portofolio perusahaan asuransi dapat menjadi hal yang mencerahkan. Pada tahun 2016, aset perusahaan asuransi diinvestasikan sebesar 67% pada obligasi (hampir seluruhnya pada obligasi korporasi dan obligasi pemerintah), 1% pada saham preferen, 12% pada saham biasa, 8% pada hipotek, 1% pada real estat, 4% pada uang tunai, 2% pada pinjaman kepada pemilik polis, dan sekitar 5% pada “lain-lain”. Berkat revolusi dana indeks, investor individu dapat membeli hampir semua barang tersebut dengan biaya kurang dari 10 basis poin per tahun. Manajemen aktif tidak memberikan hasil yang lebih baik bagi perusahaan asuransi dibandingkan dengan reksa dana.

Seperti yang mungkin Anda perkirakan, imbal hasil portofolio yang terutama terdiri dari obligasi negara (saat ini memberikan imbal hasil 1%-2%) dan obligasi korporasi (saat ini memberikan imbal hasil 3%-4%) tidak terlalu tinggi. Jadi, dari mana datangnya dividen? Sebagian berasal dari pengembalian portofolio investasi, sebagian lagi berasal dari biaya mereka yang menyerahkan polisnya, dan sebagian lagi berasal dari “kredit kematian,” yang pada dasarnya adalah uang yang tidak perlu mereka bayarkan kepada penerima manfaat karena lebih sedikit orang yang meninggal dibandingkan yang mereka rencanakan (yaitu, Anda membayar terlalu banyak untuk bagian asuransi polis karena peraturan negara). Tidak ada investasi ajaib yang dapat dilakukan oleh perusahaan asuransi yang tidak dapat Anda lakukan tanpa perusahaan. Setiap lapisan tambahan antara Anda dan investasi hanya meningkatkan pengeluaran dan menurunkan keuntungan.

Mitos #5 — Seumur Hidup Adalah Kelas Aset yang Hebat

Ada banyak kelas aset yang layak dimasukkan ke dalam portofolio yang terdiversifikasi, namun seumur hidup bukanlah salah satunya. Penjual asuransi biasanya menggunakan argumen ini ketika mereka menyadari bahwa mereka tidak dapat meyakinkan Anda bahwa seumur hidup adalah investasi yang besar. Mereka mengatakan bahwa jika Anda menggabungkannya ke dalam portofolio saham, obligasi, dan real estat, hal itu akan meningkatkan portofolio secara keseluruhan. Namun, Anda dapat menyebut apa pun yang Anda inginkan sebagai kelas aset. Kotoran kuda bisa menjadi kelas aset, tetapi bukan berarti Anda harus berinvestasi di dalamnya. Pikirkan seperti ini. Kalau saya bilang saya punya kelas aset dengan karakteristik sebagai berikut:

- Muatan depan 50% pada tahun pertama

- Menyerahkan hukuman yang berlangsung bertahun-tahun

- Membutuhkan kontribusi berkelanjutan selama beberapa dekade

- Sulit untuk menyeimbangkan kembali dengan kelas aset lain

- Didukung oleh jaminan dari satu perusahaan (dan apa pun yang bisa Anda peroleh dari asosiasi penjaminan negara)

- Mengharuskan Anda membayar bunga untuk mendapatkan uang Anda

- Jaminan keuntungan negatif untuk dekade pertama

- Pengembalian yang rendah meskipun Anda menyimpannya selama beberapa dekade

- Harus dimiliki seumur hidup untuk memberikan hasil investasi yang rendah sekalipun

- Dikecualikan dari investasi karena kesehatan yang buruk atau hobi yang berbahaya

maukah kamu membelinya? Tentu saja tidak.

Mitos #6 — Seumur Hidup Adalah Cara Hebat untuk Menghemat Pajak

Seumur hidup bukanlah cara terbaik untuk menurunkan tagihan pajak investasi Anda, rekening pensiun adalah cara terbaik. Banyak agen suka memuji manfaat pajak dari asuransi jiwa seumur hidup, sering kali membandingkannya dengan 401(k) atau Roth IRA. Nilai tunai tumbuh dengan cara yang dilindungi pajak, nilai tunai dapat dipinjam bebas pajak, dan hasil polis pada saat kematian Anda adalah pendapatan (walaupun bukan harta warisan) bebas pajak. Jadi beberapa pendukung seumur hidup menyarankan Anda menggunakan asuransi seumur hidup daripada rekening pensiun seperti 401(k) atau Roth IRA. Namun, 401(k) atau Roth IRA tidak hanya memberikan LEBIH BANYAK penghematan pajak dan memungkinkan Anda berinvestasi dalam investasi yang lebih berisiko yang mungkin memberi Anda keuntungan lebih tinggi, namun Anda juga tidak perlu meminjam uang Anda sendiri, atau membayar bunga untuk mendapatkan hak istimewa untuk melakukannya.

Saya telah memposting sebelumnya tentang 3 Cara 401(k) Menghemat Pajak Anda dan bagaimana Asuransi Jiwa Seumur Hidup Tidak Seperti Roth IRA. Saya juga telah memposting tentang bagaimana investasi hemat pajak dalam Rekening Investasi Kena Pajak tidak membawa beban pajak hampir seperti yang dikatakan oleh agen beban pajak kepada Anda. Apakah ada manfaat pajak dari berinvestasi di asuransi jiwa? Ya, tapi penjualannya terlalu berlebihan.

Mitos #7 — Asuransi Jiwa Seumur Hidup Melindungi Uang Anda dari Kreditur

Agen asuransi suka menggunakan hal ini pada dokter, yang bisa menjadi paranoid tentang masalah perlindungan aset. Namun, mereka seringkali tidak menyebutkan (atau mungkin bahkan mengetahui) bahwa undang-undang perlindungan aset sangat spesifik untuk suatu negara. Misalnya [2022] , di Alabama, hanya $500 dari nilai tunai asuransi jiwa yang dilindungi dari kreditor, namun 100% uang di 401(k) atau IRA Anda dilindungi. West Virginia hanya memberikan perlindungan $8.000. Carolina Selatan melindungi $4,000. New Hampshire tidak memberikan perlindungan apa pun. Banyak negara bagian yang memberikan perlindungan 100% untuk nilai tunai asuransi jiwa seumur hidup, namun Anda mungkin harus mempelajari undang-undang khusus negara bagian Anda sebelum terjerumus ke dalam mitos ini.

Mitos #8 — Anda Membutuhkan Seumur Hidup untuk Perencanaan Perumahan

Asuransi jiwa nilai tunai memiliki beberapa fitur perencanaan harta benda hebat yang bisa sangat berguna. Namun, sebagian besar orang, termasuk dokter, tidak memerlukan fitur tersebut. Manfaat utama asuransi jiwa adalah Anda mendapatkan banyak uang tunai bebas pajak penghasilan pada saat kematian Anda. Hal ini dapat membantu mengatasi banyak masalah likuiditas, seperti kepemilikan properti mahal atau bisnis swasta. Jika Anda mempunyai dua anak yang ingin Anda bagi warisannya secara merata, dan sebagian besar harta warisan Anda adalah tanah pertanian keluarga, maka mereka harus menjual tanah tersebut, membaginya menjadi dua, atau menyuruh salah satu anak membeli anak yang lain agar bisa dibagi rata. Namun, jika Anda juga memiliki polis asuransi jiwa dengan nilai yang sama dengan tanah pertanian, satu anak dapat memperoleh tanah pertanian tersebut dan anak lainnya dapat memperoleh hasil asuransi. Demikian pula, jika Anda beruntung memiliki tanah yang sangat besar (lebih dari $5 Juta untuk orang lajang menurut kode pajak federal, namun bisa jauh lebih sedikit di beberapa negara bagian), hasil asuransi jiwa dapat digunakan untuk membayar pajak tanah. Hal ini akan berguna bahkan bagi ahli waris tunggal untuk mencegah dia menjual properti atau bisnis berharga dengan harga jual tinggi untuk membayar tagihan pajak.

Beberapa orang juga suka menaruh asuransi jiwa dalam perwalian yang tidak dapat dibatalkan untuk mengurangi ukuran harta warisan mereka dan menghindari pajak harta benda. Meskipun Anda bisa memasukkan investasi kena pajak yang sederhana ke dalam perwalian (dan kemungkinan besar akan menghasilkan keuntungan karena tingkat pengembalian yang lebih tinggi), tarif pajak perwalian bisa sangat tinggi, sehingga memberikan hambatan yang serius pada tingkat pengembalian investasi yang tidak efisien pajak, belum lagi faktor kerumitannya. Penting untuk diketahui bahwa ini bukanlah asuransi jiwa yang menghemat uang untuk pajak properti, namun fakta bahwa Anda memberikan aset Anda sebelum Anda meninggal dengan menaruhnya ke dalam perwalian.

Namun, faktanya adalah bahwa sebagian besar orang Amerika, bahkan dokter, dan bahkan dokter dengan “masalah pajak properti,” tidak memerlukan asuransi seumur hidup untuk melakukan perencanaan properti yang efektif. Kebanyakan orang akan meninggal tanpa beban pajak properti. Di antara mereka yang perkebunannya berhutang pajak, sebagian besar mempunyai aset likuid yang dapat digunakan untuk membayar pajak. Bahkan jika Anda ingin mengurangi luas tanah milik Anda untuk mencegah pajak tanah, Anda dapat melakukannya dengan mudah tanpa membeli asuransi jiwa. Anda dan pasangan Anda masing-masing dapat menyumbang $16.000 [2022 — kunjungi halaman nomor tahunan kami untuk mendapatkan angka terbaru] kepada ahli waris mana pun pada tahun tertentu tanpa implikasi pajak warisan/hadiah apa pun. Contohnya, jika Anda mempunyai 4 anak dan mereka masing-masing mempunyai 4 anak dan 20 ahli warisnya semuanya menikah, maka jumlahnya adalah 40 orang. 40 x $16K x 2 =$1,28 Juta per tahun yang dapat diambil dari harta milik Anda tanpa membayar pajak harta benda/hadiah apa pun. Tidak perlu waktu lama untuk mencapai batas pajak properti sebesar itu, tidak perlu asuransi.

Mitos #9 — Seumur Hidup Adalah Cara Hebat untuk Membayar Biaya Kuliah

Beberapa agen bahkan menyarankan Anda menggunakan polis seumur hidup untuk membiayai kuliah anak Anda. Bisakah kamu melakukan ini? Tentu saja. Anda cukup mengambil pinjaman polis dan mengirimkan uang itu ke universitas untuk membayar uang sekolah. Tapi Anda lebih baik menabung untuk kuliah menggunakan 529 yang bagus karena berbagai alasan. Pertama, Anda sering mendapatkan keringanan pajak negara bagian dengan menggunakan 529 yang tidak tersedia untuk asuransi jiwa seumur hidup. Kedua, Anda tidak perlu meminjam uang di 529 Anda, Anda cukup menariknya. Tidak diperlukan pembayaran bunga. Terakhir, namun tidak kalah pentingnya, pertimbangkan jangka waktu tabungan kuliah. Orang tua umumnya menabung untuk kuliah dalam jangka waktu 5-20 tahun. Dengan menginvestasikan uang tersebut secara agresif, mereka dapat mengharapkan keuntungan sebesar 7%-10%. Asuransi jiwa seumur hidup memiliki pengembalian yang sangat buruk untuk jangka waktu kurang dari 20 tahun. Faktanya, sering kali nilai tunai pengembalian “investasi” Anda sepanjang hidup bernilai negatif setidaknya selama satu dekade. Penting untuk memastikan uang Anda bekerja sekeras Anda, dan uang Anda digunakan untuk liburan selama dekade pertama dalam polis seumur hidup. Pendukung seumur hidup akan mengatakan bahwa jika Anda meninggal, tunjangan kematian masih dapat membiayai kuliah Junior, namun jauh lebih murah untuk menutupi risiko tersebut dengan asuransi jiwa berjangka.

Mitos #10 — Seumur Hidup Adalah Kemewahan yang Anda Inginkan

Agen asuransi kadang-kadang akan kembali pada argumen ini ketika telah ditunjukkan bahwa klien tidak benar-benar membutuhkan tunjangan kematian permanen. Mereka mengakui bahwa klien sebenarnya tidak membutuhkan asuransi seumur hidup. Kemudian mereka mencoba menjualnya dengan alasan menjadikannya sebagai simbol status atau kemewahan. “Tentu, Anda tidak membutuhkannya, itu sebuah kemewahan.” Kemewahan menurut definisi adalah sesuatu yang tidak Anda butuhkan. Saya lebih suka kemewahan saya menjadi sesuatu yang sangat saya nikmati. Jadi sebelum membeli asuransi seumur hidup sebagai sebuah kemewahan, tanyakan pada diri Anda, “Apa yang benar-benar saya nikmati?” Jika ia memiliki asuransi seumur hidup, baiklah, belilah beberapa. Namun saya yakin sebagian besar dari kita lebih memilih kemewahan seperti mobil bagus, berlayar bersama cucu, atau mungkin sumbangan ke badan amal favorit.

Mitos #11 — Seumur Hidup Memungkinkan Anda Menghabiskan Aset Anda yang Lain, Memberikan Fleksibilitas Berharga dalam Masa Pensiun

Seumur hidup bukanlah cara terbaik untuk memastikan Anda tidak kehabisan uang, annuitasi sebagian aset Anda adalah cara terbaik. Seumur hidup bukanlah cara terbaik untuk menangani masalah kematian kedua, menyusun pensiun dan anuitas dengan benar adalah cara terbaik. Agen seumur hidup suka membuat skenario pensiun yang membuat Anda merasa harus memiliki atau setidaknya ingin memiliki asuransi jiwa permanen, terutama untuk pasangan yang sudah menikah. Misalnya, mereka akan membicarakan tentang pensiun yang hanya dibayarkan sampai pasangan yang bekerja meninggal. Atau mereka akan membicarakan tentang annuitasi sebagian aset Anda berdasarkan kehidupan salah satu anggota pasangan saja. Kemudian mereka akan menyarankan agar hasil polis seumur hidup digunakan untuk biaya hidup pasangan kedua yang meninggal. Tidak ada alasan untuk menggunakan kebijakan seumur hidup dengan cara ini. Jika Anda ingin pensiun Anda bertahan hingga Anda berdua meninggal, pilih opsi itu. Jika Anda ingin anuitas Anda bertahan hingga Anda berdua meninggal, pilih opsi itu. Ya, ia akan membayar dengan persentase yang sedikit lebih rendah, namun perbedaan antara pembayarannya lebih kecil dari biaya polis asuransi jiwa seumur hidup yang akan menutupi hilangnya dana pensiun tersebut. Ini bukanlah solusi yang tepat untuk masalah ini. Apakah asuransi seumur hidup memberikan fleksibilitas dalam masa pensiun? Tentu saja, namun biaya untuk fleksibilitas tersebut terlalu tinggi.

Mitos #12 — Seumur Hidup Adalah Cara Hebat untuk Membeli Barang Mahal

Seumur hidup bukanlah cara terbaik untuk membeli barang-barang mahal, menabung untuk itu adalah cara terbaik. Ada beberapa penjual asuransi yang sangat kreatif di luar sana yang menganjurkan sistem seperti Bank on Yourself atau Infinite Banking. Skema dasarnya adalah ini:dengan menyusun polis Anda secara tepat dengan tambahan yang dibayar, Anda mendapatkan banyak nilai tunai ke dalam polis Anda di tahun-tahun awal, sehingga Anda mencapai titik impas dalam 3-4 tahun, bukan 8-15 tahun. Anda juga membeli polis yang bersifat “pengakuan tidak langsung”. Artinya ketika Anda meminjam dari polis, perusahaan asuransi tetap membayar dividen atas jumlah yang ada sebelum Anda meminjamnya, sehingga dividen polis pada dasarnya membatalkan pembayaran bunga yang harus dibayar atas pinjaman tersebut. Sekarang, daripada pergi ke rekening tabungan Anda atau ke bank untuk meminjam uang ketika Anda membutuhkan mobil, kulkas, atau properti investasi, Anda meminjam polis seumur hidup Anda tanpa biaya apa pun. Selain itu, nilai tunai pada polis yang tidak Anda pinjam akan tumbuh lebih cepat dibandingkan uang di bank tabungan.

Jadi apa masalahnya? Masalahnya adalah Anda harus membeli polis seumur hidup yang tidak Anda perlukan. Anda mungkin mencapai titik impas lebih cepat dibandingkan dengan kebijakan tradisional, namun masih ada keuntungan negatif selama beberapa tahun dan dalam jangka panjang, keuntungan yang sama rendahnya. Apakah lebih baik memperoleh penghasilan 4%-5% setahun setelah 5 tahun atau memperoleh 1% setahun mulai tahun pertama? Nah, untuk 6 atau 7 tahun pertama Anda lebih baik menggunakan rekening tabungan 1% setahun. Selain itu, jika suku bunga naik dari posisi terendah dalam sejarah, Anda masih terikat dengan sistem ini selama sisa hidup Anda. Belum lama ini saya bisa mendapatkan lebih dari 5% dari dana pasar uang. Tampaknya juga sangat mudah untuk membiayai mobil di dealer dengan suku bunga yang sangat rendah. 0% atau 1% bukanlah hal yang jarang terjadi. Anda lebih baik meminjam dari mereka sebesar 1% daripada dari polis Anda sebesar 5%. Ini adalah masalah serupa dengan peralatan dan hipotek. Anda melakukan semua upaya ini sehingga Anda dapat meminjam dari diri Anda sendiri, kemudian menyadari bahwa meminjam dari orang lain lebih murah. Terakhir, jika Anda tidak perlu melakukan pembelian selama 5 atau 10 tahun, Anda punya waktu untuk berinvestasi pada sesuatu yang kemungkinan besar memberikan keuntungan lebih tinggi daripada polis seumur hidup. Apakah mereka yang mengandalkan dirinya sendiri akan ditipu? Belum tentu, namun pada umumnya mereka terlalu banyak menjual manfaat dari skema mereka. Pendukungnya terutama adalah agen asuransi yang ingin meningkatkan penjualan melalui pemasaran kreatif. Menabung hanyalah cara yang lebih baik untuk melakukan pembelian dalam jumlah besar dibandingkan membeli polis seumur hidup.

Mitos #13 — Orang atau Pebisnis yang Sangat Kaya Membeli Asuransi Jiwa Seumur Hidup, Jadi Anda Juga Harus

Pendukung seumur hidup, terutama mereka yang menganjurkan penggunaan polis Anda sebagai bank, ingin menunjukkan bahwa banyak orang kaya dan banyak bisnis (termasuk bank) sebenarnya membeli asuransi seumur hidup. Meskipun benar, hal ini tidak relevan bagi orang pada umumnya. Bisnis besar tidak memiliki akses terhadap opsi rekening pensiun yang menghemat pajak seperti yang dimiliki oleh individu kelas menengah. Orang-orang yang sangat kaya telah memaksimalkan hal ini. Ketika Anda memiliki lebih banyak uang daripada yang Anda perlukan, laba atas uang Anda tidak terlalu menjadi masalah. Bill Gates mampu berinvestasi pada sesuatu yang memberikan keuntungan 2%-5% karena dia tidak membutuhkan uangnya untuk bekerja terlalu keras. Hal ini tidak berlaku bagi sebagian besar masyarakat kelas menengah ke atas, termasuk dokter. Seperti dibahas di atas, orang-orang yang sangat kaya juga lebih memanfaatkan manfaat perencanaan warisan terbatas dan manfaat perlindungan aset dari asuransi jiwa permanen. Singkatnya, rendahnya keuntungan yang melekat dalam seluruh kehidupan tidak menjadi masalah bagi mereka dibandingkan bagi Anda.

Mitos #14 — Anda Harus Membeli Seumur Hidup Saat Anda Muda

Penjual seumur hidup ingin menunjukkan bahwa seumur hidup jauh lebih murah jika Anda membelinya saat Anda masih muda. Meskipun benar bahwa preminya lebih rendah jika Anda membeli polis pada usia 25 dibandingkan jika Anda membelinya pada usia 55, setelah Anda memperhitungkan nilai waktu uang dan fakta bahwa Anda akan membayar premi selama 3 dekade tambahan, investasi di usia muda tidak lebih baik daripada di usia yang lebih tua. Aktuaris adalah orang-orang yang sangat cerdas, dan untuk risiko yang relatif mudah untuk dimodelkan, seperti kematian, mereka dapat menentukan harga asuransi dengan cukup efisien.

Selain preminya yang lebih rendah, ada dua alasan lain mengapa lebih baik membelinya saat Anda masih muda. Pertama, komisi tersebut tersebar selama beberapa tahun, sehingga dampaknya lebih kecil terhadap keuntungan Anda secara keseluruhan. Namun alternatif untuk tidak membayar komisi sama sekali jauh lebih menarik. Kedua, ada kemungkinan Anda menjadi kurang sehat atau melakukan olahraga berbahaya di kemudian hari. Ini adalah salah satu kelemahan serius dalam menggunakan asuransi jiwa sebagai investasi—tidak semua orang dapat menggunakannya. Entah mereka tidak memenuhi syarat sama sekali, atau harga asuransinya sangat tinggi sehingga laba atas investasinya bahkan lebih rendah daripada yang seharusnya. Saya tidak melihatnya sebagai alasan untuk membelinya ketika Anda masih muda, saya melihatnya sebagai alasan untuk tidak membelinya sama sekali. Dapatkah Anda bayangkan jika Vanguard mengirim paramedis ke rumah Anda untuk mengambil darah sebelum mengizinkan Anda membeli dana S&P 500 mereka?

Mitos #15 — Pengabaian Penunggang Premium adalah Cara yang Baik untuk Melindungi Pensiun Anda dari Disabilitas

Asuransi jiwa seumur hidup bukanlah cara terbaik untuk melindungi pendapatan pensiun Anda dari kecacatan Anda, melainkan asuransi kecacatan. Menyadari bahwa premi asuransi jiwa seumur hidup sangat mahal dan akan sulit diperoleh jika Anda mengalami kecacatan, perusahaan asuransi mulai menawarkan pengendara yang membebaskan premi jika Anda mengalami kecacatan. Kadang-kadang Anda bahkan tidak perlu membayar ekstra untuk manfaat ini. Mereka yang menyukai taktik ini kehilangan beberapa poin. Pertama, jaminan tidak gratis. Setiap jaminan dikenakan biaya dalam bentuk pengembalian yang lebih rendah, baik perusahaan asuransi mengenakan biaya tambahan untuk jaminan tersebut atau “memasukkannya ke dalam polis” sehingga disembunyikan.

Kedua, asuransi disabilitas itu rumit dan definisi disabilitas itu penting. Kebanyakan dokter yang menginginkan jaminan disabilitas menghabiskan banyak uang untuk mendapatkan polis yang bagus dengan definisi disabilitas yang luas termasuk cakupan “pekerjaan sendiri” karena mereka ingin memastikan perusahaan harus membayar jika mereka mengalami disabilitas. Kebijakan asuransi seumur hidup tidak begitu komprehensif dan kecil kemungkinannya untuk dibayar di wilayah abu-abu yang sering kali menjadi bagian dari disabilitas. Anda hampir pasti akan lebih baik membeli polis disabilitas yang lebih besar daripada pengecualian asuransi premium seumur hidup. Asuransi kecacatan Anda mungkin juga menawarkan perlindungan pensiun. Meskipun hal ini juga memiliki masalah (terutama dalam cara pembayaran manfaatnya), hal ini lebih baik daripada mencoba mendapatkan asuransi kecacatan dari polis seumur hidup.

Jika Anda merencanakan pensiun dini seperti saya, Anda mungkin menyadari bahwa Anda tidak memerlukan perlindungan disabilitas untuk melindungi iuran pensiun Anda, setidaknya setelah beberapa tahun menabung dalam jumlah besar. Pertimbangkan untuk memiliki portofolio senilai $750K pada usia 40 tahun. Anda memperkirakan bahwa Anda membutuhkan $2 Juta dalam dolar hari ini untuk masa pensiun. Anda berencana untuk menabung dalam jumlah besar sehingga Anda dapat mencapainya pada usia 50 dan pensiun. Apa rencana cadangannya jika Anda menjadi cacat dan tidak dapat menyimpan semua uang itu? Asuransi kecacatan Anda tidak hanya membayar hingga usia 50 tahun. Asuransi ini juga membayar hingga usia 65 tahun. Jadi, Anda tidak memerlukan portofolio Anda untuk menanggung 15 tahun tersebut. Anda juga dapat mulai menerima pembayaran Jaminan Sosial pada saat pembayaran disabilitas habis. Karena Anda tidak perlu menyentuh portofolio Anda, portofolio dapat terus berkembang. Jika ia tumbuh sebesar 5% setelah inflasi, pada saat Anda mencapai usia 65 tahun, nilainya akan lebih dari $2,5 Juta dalam dolar saat ini. Jangan membeli asuransi yang tidak Anda perlukan. Namun bahkan sebelum Anda memiliki portofolio apa pun, cara terbaik untuk melindungi tabungan pensiun Anda adalah dengan membeli LEBIH BANYAK asuransi kecacatan, bukan mencoba mendapatkannya dari polis seumur hidup. Bahkan jika Anda dapat menggunakan pertanggungan tambahan untuk menyediakan portofolio pensiun Anda, Anda harus dapat memasukkannya ke dalam investasi dengan tingkat pengembalian yang tinggi, yang kemungkinan besar tidak akan diperoleh seumur hidup. Rekening kena pajak yang diinvestasikan secara agresif baik-baik saja karena penghasilan utama Anda jika dinonaktifkan, manfaat asuransi kecacatan Anda, bebas pajak.

Mitos #16 — Anda Harus Menukar Polis Seumur Hidup Lama Anda yang Buruk dengan Polis Baru yang Mengkilap

Karena agen mendapat komisi baru setiap kali dia menjual polis baru, meskipun dia mengganti polis lama dari perusahaan yang sama, dia mempunyai konflik kepentingan yang serius dalam memberikan rekomendasi kepada Anda. Saya berinteraksi dengan banyak agen asuransi di blog ini, dan tidak satupun dari mereka setuju dengan yang lain tentang apa itu polis seumur hidup yang “terstruktur dengan baik”. Artinya, jika Anda pergi ke agen kedua, dia hampir pasti akan memberi tahu Anda bahwa ada cara yang lebih baik untuk melakukannya. Namun, agar pertukaran satu kebijakan dengan kebijakan lain bisa bermanfaat, kebijakan awal harus benar-benar buruk, terutama setelah beberapa dekade. Alasannya adalah rendahnya tingkat pengembalian asuransi seumur hidup terkonsentrasi pada tahun-tahun awal. Saya melihat sebuah kebijakan baru-baru ini. Ini ditetapkan sebagai investasi dengan tambahan yang dibayarkan untuk 25 tahun pertama. Itu adalah upaya terbaik agen dalam memaksimalkan keuntungan dari suatu polis. Berikut tampilan imbal hasil tahunannya:

Dijamin Diproyeksikan 10 tahun pertama-1,84%0,98%15 tahun berikutnya2,55%5,47%25 tahun berikutnya1,99%5,13%Hal ini menunjukkan bahwa kelompok masyarakat miskin sangat terkonsentrasi pada tahun-tahun awal. Dengan kebijakan khusus ini, keuntungan sebenarnya menurun setelah 25 tahun karena pada saat itulah Anda berhenti melakukan penambahan pembayaran. Dengan kebijakan yang lebih tradisional, baris ketiga akan sedikit lebih tinggi dibandingkan baris kedua. Namun pesan moral dari cerita ini adalah Anda harus membeli “polis yang tepat” terlebih dahulu, dan bahkan polis jelek yang sudah berumur lebih dari 10 tahun akan lebih baik daripada polis baru yang lebih baik. Ini juga merupakan alasan mengapa sebaiknya tetap mempertahankan polis seumur hidup yang lebih tua, meskipun membelinya pada awalnya adalah sebuah kesalahan. Penting juga untuk melihat seberapa kecil risiko yang sebenarnya diambil oleh perusahaan asuransi, karena perusahaan asuransi bahkan tidak menjamin bahwa nilai tunai Anda akan mampu mengimbangi inflasi.

Mitos #17 — Seumur Hidup Adalah Satu-satunya Cara untuk Memberikan Uang kepada Ahli Waris Bebas Pajak Penghasilan

Seumur hidup bukanlah satu-satunya cara untuk memberikan uang kepada ahli waris bebas pajak penghasilan pada saat kematian Anda. Faktanya, ini bukanlah cara terbaik, Roth IRA adalah cara terbaiknya. Ketika Anda meninggal, ahli waris Anda mendapatkan manfaat asuransi kematian yang bebas pajak penghasilan. Apa yang sering tidak disebutkan oleh agen adalah bahwa semua yang diperoleh ahli waris dari Anda ketika Anda meninggal adalah bebas pajak penghasilan. Berkat peningkatan basis saat kematian, segala sesuatu di luar rekening pensiun, termasuk furnitur, mobil, saham, uang tunai, reksa dana, dan real estat semuanya dinilai kembali pada hari kematian Anda. Karena basisnya sekarang sama dengan nilainya, tidak ada pajak capital gain yang harus dibayar. Mewarisi rekening pensiun bisa lebih baik lagi, terutama rekening Roth yang pajaknya sudah dibayar. You can take all the money out the same year you inherit it and not pay any taxes at all. Or, you can “stretch it”, taking withdrawals gradually over decades until you die. Meanwhile, it continues to grow tax-free. You can stretch an inherited tax-deferred account too, but you do have to pay taxes on any money withdrawn from the account.

Myth #18 — With Whole Life, There Is No Way I Can Lose Money

People invest in whole life insurance because they like guarantees. The insurance company guarantees that you'll get a certain rate of growth on your investment and it guarantees a death benefit. The guarantees, however, aren't worth nearly as much as people often assume. For instance, the guaranteed scale of any whole life insurance policy guarantees that your money will grow slower than the historical rate of inflation, despite sticking with it for half a century. Before deciding to trust a single company with your life savings, you might want to consider what happens if it goes out of business. There are state insurance guarantee associations that will cover the cash value and death benefit of your policy, but how much will they really cover? You might be surprised how little it is. In my state, only $500K in death benefit and $200K in cash value is covered, NO MATTER HOW MANY POLICIES YOU OWN. Your state is probably similar. No wonder agents are always talking about the long-term viability of their insurance company. It really does matter! Now I don't think the risk of any given insurance company going out of business in any given year is very high, nor do I think a typical purchaser is likely to end up with exactly the guaranteed growth rate. But before buying, you should realize that investing in whole life insurance isn't the risk free proposition agents like to present it as.

Myth #19 — Life Insurance Should Not Be “Rented”

This one is pretty easy to see through, but you still see agents using it frequently. Since everyone “knows” that it is better to own a home than rent one, the agent says something like “You wouldn't rent your home for the rest of your life would you? So why would you rent your life insurance?” Basically, the agent is referring to the fact that if you use term insurance after age 60 or so, it becomes more and more expensive each year, just like renting a home. But unlike a home, you don't need life insurance after you become financially independent. When you only need a home for a year or two or three, it is a better idea to rent than to buy. When you only need life insurance for a decade or two or three, it is also a better idea to “rent” than to buy. The opportunity cost of “ownership” is simply too high.

Myth #20 — Banks Own Life Insurance So You Should Too

This is a frequent one heard from the Bank on Yourself/Infinite Banking crowd. An underpinning of this school of thought is that the greedy banks are taking over the world so you should only do your financial work through the trustworthy insurance companies. To be honest, I don't have massive distrust for either one of these industries. Both industries have mutually-owned options (mutual life insurance companies and credit unions) where, like Vanguard, the customers own the company. The agents like to point out that banks actually own whole life insurance as part of their “Tier One Capital,” the money used to determine if the bank is adequately capitalized or not. This is somehow to make you fear that the banks know something you don't, like the financial world is about to implode and any of those using banks instead of insurance companies for their financial needs are going to go broke. Tier One Capital is a measure of a bank's financial strength. Banks use less than 25% of their Tier One Capital to buy single premium whole or universal life insurance on a group of employees. The bank owns the policy and is the beneficiary. When the employee keels over, the bank gets the cash. The bank is buying the policy primarily for the death benefit, not because the return is particularly high.

Tier One Capital is highly regulated and it is difficult for a bank to include riskier assets such as common stock(aside from that of the bank, which makes up most of Tier One Capital) and REITs in its Tier One Capital. When you are stuck choosing between low-risk/low-return investments, then you can understand why a bank might consider something like cash value life insurance with part of that money. However, individual physician investors investing for retirement have fewer restrictions on their investment options for their retirement. Most of them have significant need for their retirement money to grow. The returns available with cash value life insurance generally are not high enough for them to reach their goals. Even so, consider what a bank does with most of its Tier One Capital—it buys the only stock it can, it's own. If whole life insurance was so awesome, you'd think the bank would use all of its Tier One reserves to buy it. In short, doctors aren't banks, so doing what banks do isn't necessarily smart. Tier One Capital is highly regulated and it is difficult for a bank to include riskier assets such as common stock.

Myth #21 — Corporate CEOs Own Whole Life Insurance So You Should Too

Agents, particularly of the Bank on Yourself type, love to point out that the golden parachutes for many highly-paid CEOs include cash value life insurance policies. However, just as the financial situation of a bank is dissimilar from that of a physician, so is the financial situation of a CEO making $10 Million a year different from that of a physician. When you're making a gazillion dollars a year, rate of return on your money becomes much less important and thus the benefits of whole life (asset protection, tax, estate planning, etc.) become relatively more important. It isn't that returns on whole life magically get better. Again, if you are in a position that you only need your long-term money to grow at 3%-5% nominal per year, then feel free to invest in whole life insurance. Most of us, however, need higher growth. Remember that a doctor making $200,000 per year and a CEO making $10 Million per year are in very different financial circumstances and what works fine for one will not necessarily work well for the other.

Myth #22 — Banks Failed During The Great Depression, But Insurance Companies Didn't

This myth again preys on the fears of a global economic meltdown. In 1933 there were two holidays. The first was a “Banking Holiday” in which the banks were closed for 10 days as sweeping regulatory changes took place. The second was an “Insurance Holiday” in which for a period of nearly six months you could neither surrender your cash value life insurance policies for cash, nor borrow against them. Aside from this holiday, 14% (63 companies) of life insurance companies actually DID fail during The Great Depression. In fact, if they would have actually marked to market the bonds and mortgages they held, they would have ALL been insolvent. Reforms were put in place during The Great Depression that fixed many of the problems leading to bank failures and the banking holiday. However, these reforms were never put in place for insurance companies.

Myth #23 — After-Tax, Whole Life Returns Are Better Than Bond Returns

This one usually goes like this. “If you can buy a bond yielding 5% and are in a 45% marginal tax bracket, the after-tax yield on that is just 2.75%. A whole life policy with a “tax-free” internal rate of return of 5% is better.” This is an apples to oranges comparison. What is the 1 year return on that whole life policy? 2.75% sounds a whole lot better to me than a -50%. Even at 10-20 years, the bond is still way ahead.

I wrote about a physician who was pleased with his 7% return on his whole life policy bought in 1983 (don't expect to see that again any time soon). Except that he could have bought a 30-year treasury that year yielding 10.5%. 10 years later, as his whole life policy is breaking even and interest rates have dropped, the bond purchaser has not only already more than doubled his money just from the coupon payments, but the capital gains on that bond added another 50% to his return. That investor would have done even better purchasing equities in 1983, the start of an 18 year bull market. A bond, which can be sold any day the market is open, simply cannot be compared in any fair manner to an insurance policy which must be held for life to have any decent kind of return. Besides, most physician investors can hold taxable bonds inside retirement accounts instead of a taxable account anyway. That retirement account not only provides for tax-protected growth like a whole life policy, but also a tax-rate arbitrage between your marginal rate at contribution and your effective rate at withdrawal, further boosting returns.

Even if your only choice is between buying bonds in a taxable account and buying whole life insurance, keep in mind that even at today's low interest rates you can still buy Vanguard's Long-Term Tax Exempt Muni Fund yielding 3.17% [2014] . The guaranteed return on whole life insurance cash value, held until your life expectancy, is about 2% and the projected return is only ~5%. Realistically, you should probably expect a return of 3%-4% over the long term on that policy. Of course, if you actually wish to cash out of that policy instead of borrowing from it (and paying interest for the right to borrow your own money), the earnings are just as taxable as any taxable bond fund. And if you want your money in a mere 10-20 years, you're going to come out way behind with the life insurance.

Now, if you really understand how whole life insurance works and you think its unique features outweigh its significant downsides, then feel free to run out and purchase as much as you like. It truly does not bother me. I do not make any money if you buy whole life, nor if you decide to buy something else. However, if you are like most, once you understand it, you won't buy it and in fact, if you already have, you'll probably be looking for the best way to get out of whole life insurance. Don't feel bad. 80% of those who purchase these policies surrender them prior to death, 36% within just five years. You've got to ask yourself why so many people who were apparently intending to hold this product for the next 40 or 50 years suddenly changed their mind. I'm sure it has nothing to do with it being inappropriately sold to the financially unsophisticated by insurance agents facing a terrible financial conflict of interest with their clients. Whole life insurance is a product made to be sold, not bought. It is a solution looking for a problem that exists for very few, if it exists at all.

Myth #24 — Whole Life Insurance Keeps Assets Off the FAFSA

This is one is merely misleading. The statement as it stands is true. The Free Application for Federal Student Aid (FAFSA) does NOT consider whole life insurance cash value as an asset of the student or the parents. The problem is, for the typical reader of this blog, that it doesn't matter. Your income alone will keep your child from qualifying for any need-based college financial aid. So if you buy a whole life policy for this reason, you're likely to be disappointed.

Myth #25 — Term Life Expires Without Paying Anything

Another misleading argument. I'm always surprised to see people fall for this line, but they do. Do you complain when you don't get to use your car insurance for any given six month period? How about when your house doesn't burn down? Or you don't get cancer and get to use your health insurance? Then why in the world would you complain that your term life insurance expires and you're still alive. Term life insurance is pure insurance. If you die, it pays. If you live, it doesn't. As a general rule, since on average insurance must cost more than it pays out (since insurance companies have both expenses and profits), you should insure against financial catastrophes. When it comes to death, the financial catastrophe is dying during your earning years, before you become financially independent. So that's the only time period you need to insure against. Some people only fall halfway for this argument, and buy return of premium term life insurance. The same principle applies, of course. You don't walk away empty-handed when your term life policy expires. You had insurance for the entire term, which is exactly what you needed.

Myth #26 — Whole Life Insurance Is the Perfect Investment

This outright lie comes from the true believers. They argue that whole life insurance is safe, liquid, tax-advantaged, creditor-proof, and offers a competitive return. These half-truths all add up to one big lie. Let's take them one at a time:

#1 Safe

Safe from the cash value going down, perhaps, but not safe from losing money. A huge percentage of whole life insurance purchasers lose money because they cancel the policy at some point in the first 5-15 years before they break even on their “investment.”

#2 Liquid

I guess it's more liquid than owning a website or a rental property, but it pales in comparison to the liquidity available in a savings account or a mutual fund that can be liquidated any day the market is open. Even inside retirement accounts, there is absolute liquidity after age 59 1/2, and fair liquidity even prior to that date. Most of the time with whole life insurance you don't even get your money, you just have the right to borrow against it at pre-set terms. You can get that with a HELOC.

#3 Tax-Advantaged

Few understand just how minor the tax advantages of whole life insurance are. There is no up-front deduction like a 401(k). Unlike a real investment, there are no capital gains rates if you surrender a policy with a gain and you cannot deduct the loss if you surrender it with a loss (the usual case). You don't get to use depreciation to reduce the tax burden of your income like with real estate. Instead of being able to withdraw the money tax-free like with a Roth IRA, you can only borrow against the policy, and that's tax-free but not interest-free, just like borrowing against your house, car, or mutual fund portfolio. Sure, you don't pay taxes on the “dividends,” but that's because they're actually a return of premium (i.e., you paid too much for the insurance). The only real tax break associated with life insurance is that the death benefit is tax-free. But that isn't any different from any other investment, where you get the step-up in basis at death. In addition, whole life can't be stretched like an IRA. The tax benefits, such as they are, are limited to a single generation.

#4 Creditor-Proof

Too few docs understand just how low the risk of needing this protection actually is. I calculate my risk of being successfully sued for an amount above policy limits at 1 in 10,000 per year. Maybe half that now that I'm practicing half-time. So should I be so unlucky as to be that one person, I would declare bankruptcy and be left only with protected assets. In my state, that's my retirement accounts, my spouse's assets, $40,000 in home equity, and whole life insurance cash value. Your state may or may not protect whole life insurance cash value. Please actually check if you are so paranoid to actually buy whole life insurance for this reason.

#5 Competitive Return

Apakah kamu bercanda? Competitive with what? Whole life insurance generally has a negative return for 5-15 years (sometimes more than 30 for really terrible policies). Even a good policy held for 5+ decades only guarantees a 2% return and projects a 5% return.

If I were going to draw up the perfect investment, it would definitely avoid the following characteristics of whole life insurance

- Guaranteed negative return for years

- Requirement to interact with and pay a commission to an insurance agent

- Requirement to give samples of body fluids and submit to a medical exam

- Requirement to answer pesky questions about my health

- Requirement to avoid risky activities

- Requirement to pay interest in order to use my own money

It only qualifies as an “okay” investment in certain very limited situations. It's not even close to a perfect one.

Myth #27 — Insurance Agents Are Just People

This is one of my favorites to see in any sort of discussion with an insurance agent about the merits of whole life insurance. It usually comes when I point out that my problem with whole life insurance isn't so much the product as the way in which it is sold. Obviously, many of them take that quite personally since they've dedicated their life and career to selling this product inappropriately. So they point out that there are bad doctors or that insurance agents are just people trying to make a living. I don't have a problem with the sales profession. I don't even have a problem with people earning commissions for selling stuff. Cindy gets paid on commission to sell ads right here at The White Coat Investor. But if you seek advice from Cindy about whether buying an ad at The White Coat Investor is a good idea for you, you're a fool. Insurance agents are just people and people respond to incentives. An insurance agent has a huge incentive to sell you a whole life policy. The commission on a policy is 50%-110% of the first year's premium. Now you know why he's trying so hard to sell you a big fat doctor policy.

Myth #28 — No 1099 Income with Whole Life

This was a new one to me. I thought I had heard every possible argument for buying a whole life policy until someone whipped this one out. How much trouble is it for you to deal with a 1099? It takes me about 30 seconds using Turbotax. Certainly not a reason to favor one investment over another. Remember not to let the tax tail wag the investment dog. Your goal isn't to minimize your taxes or maximize your tax-free income. It's to have the most money AFTER paying the taxes due.

Myth #29 — What Does The White Coat Investor Know? He's Just a Doctor, and Probably a Crappy One

Sometimes agents start with this argument, but frequently this is where they end, with ad hominem attacks. Sometimes it's phrased like one of these:

So, exactly how does being an ER doctor qualify you to give financial and insurance related advice?

Do everyone a favor and stick to studying medicine.

You’re young, a doctor and absolutely sure that you know everything.

Obviously, medicine has lots of problems and doctors don't know everything, but if the agent's best argument for whole life insurance is an ad hominem attack, that's a good sign that you should have stood up and walked out a long time ago.

Myth #30 — After Maxing Out a 401(k) and Roth IRA, Isn't Whole Life Insurance the Only Tax-Sheltered Option Left?

This is the wrong question to be asking, but the answer to it is still no. Just because it is the only option presented to you by an insurance agent, doesn't mean it is the only option. Other options for retirement savings include defined benefit/cash balance plans, an individual 401(k) for self-employment income, a spousal Roth IRA, your spouse's employer-provided accounts, and Health Savings Accounts (HSAs). In some ways doing Roth conversions and paying off debt is also tax-sheltered. But most importantly, there is no limit on investing in a non-qualified mutual fund account (where long-term gains and qualified dividends are somewhat sheltered from taxes) or in real estate (where income is sheltered by depreciation and capital gains can be deferred indefinitely by exchanging).

Obviously investing in whole life insurance compares better to investing in a taxable account than to a retirement account (where there is no comparison from a tax, investing, or in most states an asset protection standpoint). But the real problem with this argument is that it is focused entirely on the idea that any tax-advantaged investment is always better than any fully taxable investment. That simply isn't true. It also mixes up the idea of an investment and an account, two things that financially naïve doctors sometimes have a hard time telling apart. (Think of the accounts as different types of luggage and the investments as different types of clothing.) The real question to ask yourself when you hear this argument is “Where should I invest after maxing out my available retirement accounts?” The answer is a taxable, non-qualified account. Now you're left with the question of what long-term investment to invest in—tax-efficient mutual funds, real estate, or whole life insurance? It's pretty hard to really compare the merits of those three investments and end up choosing whole life insurance given its limitations and terrible returns previously discussed.

Myth #31 — The Estate Tax Exemption Could Go Down

The idea behind this argument is a rebuttal to the argument discussed in Myth #8. In summary, that argument is that you need whole life to avoid estate taxes, which is silly given the vast majority of doctors won't owe any federal estate taxes. The next step is for the agent to argue “Well, the estate tax exemption might be decreased.” Well, I suppose that's true. Congress can change any law they want any time they want. But buying insurance or investing based on what could happen seems foolhardy. I mean, it is probably just as likely that the estate tax is eliminated as the exemption reduced. It seems to me the best way to plan for the future is to project current law forward, since most laws aren't going to be significantly changed. If they are, you can make changes at that point. At any rate, it isn't like whole life insurance is some magic panacea to eliminate estate taxes. The only reason whole life insurance reduces your estate taxes is by making sure you have less money due to its low returns! The thing that reduces the size of your estate is the irrevocable trust you put the insurance into, and you don't even have to put insurance into it if you don't want to.

Myth #32 — Whole Life Insurance Protects from Nursing Home Creditors

This one was particularly fun to debunk. Apparently, the idea here is to not pay for your own nursing home care somehow by purchasing whole life insurance instead of mutual funds. I'm not sure exactly how those envisioning this process think it will go. Maybe they think the nursing home doesn't ask for money until after you die or something, which is, of course, completely silly. But I think what they're referring to is the ability to spend down your assets to Medicaid levels, get Medicaid to pay for the nursing home, and still be able to leave a huge inheritance to your heirs because Medicaid somehow doesn't look at the value of your whole life insurance.

The whole process of Medicaid planning is a little distasteful to me to be honest. The idea is to hide someone's assets from the state so that the heirs can have them, foisting the cost of caring for the owner of those assets on to the public. But even assuming that you have no ethical problem with doing this, it's unlikely to work very well. Medicaid is state law, so it varies by state, but in Utah, a person can have up to $2,000 in countable assets and still qualify for Medicaid. Above that level, no Medicaid until you spend down to that level. If there is a spouse, the spouse can keep 100% of assets up to $24,720 and 50% of assets up to $123,600. Above that, Medicaid won't pay for the nursing home. Non-countable assets in Utah include:

- Your home if your spouse lives in it

- The value of one vehicle (including a Tesla)

- Funds set aside for a funeral

- Household and personal items

- Cash value of your life insurance policies IF the total face value of all policies is <$1500

So I guess if you want to hide money from Medicaid in Utah, then you could go buy a $1,000 whole life policy. Most states have similar policies regarding cash value life insurance. Even if there were a state with a higher limit than Utah, this seems silly for someone who should spend her entire retirement as a multimillionaire to be making plans to spend down to Medicaid levels for nursing home care. A far better plan to stiff your fellow Utah taxpayer (assuming you have a spouse who doesn't need care) is to upgrade your house and your car.

Myth #33 — WCI Doesn't Understand the Opportunity Cost of Borrowing Against Whole Life Insurance and Investing Elsewhere

This statement has been made without explanation, but the idea isn't that complicated (nor misunderstood by WCI). You can borrow against the cash value in your whole life policy and use that money for whatever you want. You can spend it or you can invest it. Lots of whole life fans use fun phrases like “velocity of money” to describe buying a whole life policy, borrowing the money out, and investing it in something else. The really talented salesmen get you to invest it (along with any home equity they can get you to borrow out) in yet another insurance product.

Is there a cost to not maximally leveraging your life in this manner? Sure, anytime you can borrow at a lower rate and earn at a higher rate you'll come out ahead. But leverage works both ways, and the risk is not insignificant. What is not often mentioned by those advocating doing this is the opportunity cost of plunking money into a low return life insurance policy and buying unneeded death benefit instead of a higher returning investment. For instance, consider two options. You can invest $10K a year into an investment that returns 10% per year or you can buy a whole life policy that won't break even for 10 years. After 10 years, the first investment is worth $175K and the whole life policy only has a cash value of $100K. That's a $75K opportunity cost that apparently the “insurance agent doesn't understand.”

With a properly structured policy, you can break even in perhaps five years (maximizing the use of Paid-Up Additions), and using the combination of wash loans (interest rate to borrow against the policy =dividend rate of the policy) and a non-direct recognition policy, this idea becomes “not terrible.” You still have the opportunity cost of the first few years in the policy, but that is balanced out by a higher return on your cash in later years. I have discussed “Bank on Yourself” or “Infinite Banking” previously in detail if you are interested. It's not an insane use of whole life insurance, but it isn't for me. If you really understand how it works (it's going to take working through a lot of hype to do so) and want to do it, go for it.

Myth #34 — Buy Whole Life Insurance for the Long Term Care Rider

In recent years, insurance companies are adding on a Long Term Care rider to whole life insurance policies (and universal life policies and annuities) and agents are using the fear of expensive long term care to sell them. I find this appalling. Not only are you mixing insurance and investing, but you're now combining two different types of insurance policies with investing. Given the track record of insurance companies with long term care, I think most of my readers should strive to get a place where they can self-insure the risk of long term care, but even if they cannot, I'd prefer a simpler long term care policy on its own than mixing it with an otherwise unnecessary and expensive insurance policy.

The benefit of buying this as a rider of a whole life policy is that the premiums of the policy are guaranteed—you don't have the risk of the insurer upping the premiums like you do with a long term care policy or upping the cost of the underlying insurance like you do with a universal life policy. Those guarantees are worth something.

Remember we're not talking about just an accelerated death benefit. This is just another way of self-insuring long-term care, but with a lower return on the investments used to pay for it. You're really buying two policies combined into one. But there's no free lunch here. You're either paying more for the combined policy, or you're getting less of something, usually death benefit. Most likely, you're also paying for a life insurance policy you don't need or wouldn't otherwise buy. That death benefit isn't free. The reason life insurance companies stopped selling long term care insurance and started selling these hybrid policies is that their actuaries were convinced they are more likely to make money that way. That profit has to come from you, there is no other possible source.

If you do decide you wish to purchase some sort of long term care insurance policy, it is entirely possible that a hybrid product is right for you, but just like health and disability insurance, the devil is in the details. Read the fine print and be sure you know what guarantees the insurance company is actually providing. Know about what is covered, what isn't covered, and whether benefits are indexed to inflation or capped. Or better yet, live like a resident for 2-5 years out of residency so you'll be rich enough to self-insure this risk and never have to make this decision.

Myth #35 — We Don't Say Put All Your Money into Whole Life Insurance

This argument is simply bizarre, but used by agents once the prospective buyer has refused to buy the massive policy they were offered at first. A small commission is better than no commission, I guess. Of course, you shouldn't put all your money into whole life insurance, that's a straw man argument. Also, if buying a policy is a bad idea, you're going to be better off if you buy a small one than a big one. But that's hardly a reason to buy a policy in the first place. Like any asset class, if it isn't a good idea to put a significant chunk of your portfolio into it, it probably isn't a good idea to put any of your money into it.

Myth #36 — Yes, We Have a Few Bad Eggs But Most of Us Are Ethical

This argument is used when I point out that literally hundreds or even thousands of my readers have been sold clearly inappropriate insurance policies. The problem is there are two options to explain this phenomenon. The first is that these agents are unethical. The second is that they're incompetent. Given the statistic that 80% of policies are surrendered prior to death and 76% of the docs I've surveyed regret their purchase, this is hardly just a “Few Bad Eggs” doing this. It's an industry-wide problem.

Myth #37 — You Should Buy Insurance to Preserve Insurability

This one is used to sell insurance to people that don't even have a need for insurance. The idea is to prey upon their fear of the combined risk of needing insurance AND not being able to purchase it. One example would be a 25-year-old single doc with no kids. No life insurance need here. “But what if you get diabetes before you get married and have kids? You should buy the policy now.” Uhhhh . . .no.

First, you may never have dependents.

Second, if you do need it, you'll probably be able to buy it at that time at a reasonable price.

Third, if you do become less insurable, you will still likely have options for some insurance through an employer or other groups.

Fourth, even if you become uninsurable through anyone, the risks must be multiplied. For example, let's say there's a 5% risk of you becoming uninsurable before you have a real insurance need. And the risk of you dying before reaching financial independence is 5%. To get your true risk of a financial catastrophe, you must multiple those risks. 5% x 5% =0.25%. That is a 1 in 400 chance. Life is risky. You can't eliminate every possibility of something bad happening to you and even if you could, that wouldn't be a wise use of your money. Wait to buy insurance until you have a need for that insurance.

This argument is often even extended to children. If you're buying life insurance from the same company that sells you baby food, you're probably doing something wrong. Now, if you could buy a lot of future insurability for that kid very, very cheaply, that might be something to consider. Unfortunately, you can't really do that for several reasons:

First, you have to actually buy unneeded insurance. That newborn likely won't have any need at all for life insurance for 25-30 years.

Second, you're not pre-buying the policy that kid will need. You can't buy the right to buy a 30-year level term policy at age 30. You have to buy a whole life insurance policy. Which means you're also paying for insurance that will be unnecessary on the far end of life too, after the kid has become financially independent.

Third, you generally can't buy enough insurance, or even enough future insurability, to actually meet any sort of realistic life insurance need. Most of these infant policies are only $10K or so. That's basically a burial policy, and as sad as it would be to bury your kid, it's not a financial risk my readers should need to insure against. (I've even heard the argument that you should buy the policy so you can take a few months off work because you'll be too distraught to work, but that's what an emergency fund is for.) Even if you find a policy that allows you to purchase future insurability for a larger policy, let's say $500K, that's not going to mean much in 30 years when the life insurance need actually shows up for the first time, much less in 50 years when the kid is actually reasonably likely to die. At 3% inflation, $500K today will only be worth $200K in 30 years and $109K in 50 years. Better than nothing, but you went to all this effort and expense to preserve insurability and your kid still ended up with inadequate life insurance coverage.

Myth #38 — Whole Life Insurance Is a Great Investment to Put in Your Defined Benefit/Cash Balance Plan

I had this one pitched to me by a doc turned financial advisor of all people. The argument was that you could buy whole life with pre-tax dollars and then if you wanted to pull the policy out of the defined benefit plan you could do so. He felt this was an “advanced technique” for “high net worth folks.” I was flabbergasted. It was such a stupid idea I couldn't believe it. A defined benefit/cash balance plan already provides tax protected growth and asset protection, two reasons frequently cited to buy whole life insurance. You're now paying twice for those benefits. To make matters worse, should you die while this policy is in the defined benefit plan, part of the death benefit becomes taxable, negating another usual advantage of life insurance—a completely tax-free death benefit. But the main reason why this is such a stupid idea is when it comes time to close the defined benefit plan, which is usually done every 5-10 years or so in order to roll it into an IRA. At that point, you have to do one of two things.

First, you can surrender the policy and move the cash surrender value into the IRA. But what is the investment return on the first 5-10 years of a whole life policy? You break even if you're lucky. Not exactly a great investment for that time period, especially compared to a typical conservative mix of stocks and bonds.

Second, you can purchase the policy from the plan. Of course, you have to do that with AFTER-TAX dollars. So while you initially bought it with the pre-tax dollars in the plan, eventually you're going to have to cough up after-tax dollars for the policy. And then what are you left with? A whole life policy you probably neither want nor need and perhaps even with associated premiums you have to make each year. Some deal!

Myth #39 — More Money Is Passed Through Life Insurance

This myth showed up in a comment on a post on this blog. I thought it was particularly creative, especially with the way it was combined with Myth #8 (You Need Whole Life to Help For Estate Planning) and Myth #25 (Term Life Expires Without Paying Anything):

More money is passed through life insurance than any other way. I’ve seen too many people out live term which is throwing money away and need life insurance and are at that time in life uninsurable. Life is really used well in estate and trust planning.

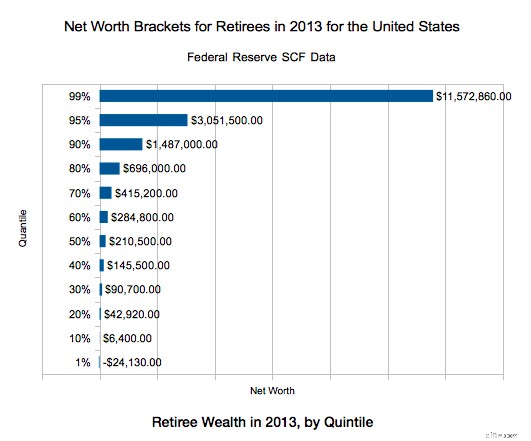

Surprisingly, this was the first time I had heard this argument. Being financially literate, of course I was able to immediately debunk it, but I suppose somebody might fall for it. There are two problems with this statement. First, it may not even be true. I looked and looked and looked for a study that showed what assets are actually inherited, without finding anything that actually quantified it. So if there is a study that actually says this, I suspect it is paid for by a life insurance company. Maybe it's true, maybe it's not, but I suspect it isn't given how few people have life insurance in force at their death. I suspect more money is left behind in houses than anything else. I mean, look at the net worth of people by age. Among retirees, the 50th percentile for net worth is $210K. That's got to be mostly house. The 80th percentile is $696K. That's about the average price of a house in my upper middle class neighborhood in a flyover state.

That jives with the average estate left behind at death:

- The average retired adult who dies in their 60s leaves behind $296K in net wealth,

- $313K in their 70s, $315K in their 80s

- $283K in their 90s

It seems very unlikely that the main inheritance most people receive is the proceeds of a life insurance policy given those numbers. How many retirees even carry life insurance? According to this, about 65% of those 65+. But 47% of those own less than $100K of life insurance. It is a well known statistic that fewer than 1% of term life insurance policies pay out. It isn't that the insurance companies aren't good for the money, it's just that people out live the term. A lesser known statistic is that 80%-90% of whole life insurance policies don't pay out either. They're surrendered prior to death, often at a loss since 1/3 of policies are surrendered in the first 5 years and over half in the first 10 years.

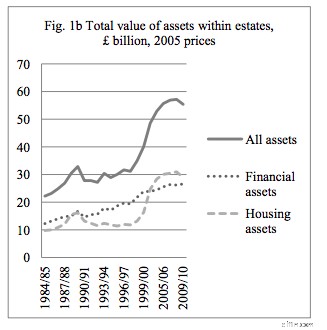

I did manage to find some UK data, however, which suggests my hunch (that people inherit more in real estate than life insurance proceeds) is correct.

As you can see, more than half of inherited assets are housing assets, so clearly more assets cannot be passed as life insurance than anything else.

Perhaps the agent wasn't referring to the median inheritance though. Perhaps he was referring to the total amount of dollars passed to heirs. I could find no data to support nor refute that notion.

Second, even if the statement is true, it is irrelevant. Given that THE PURPOSE of life insurance is to pass assets on to heirs, that's hardly an argument to buy life insurance for some reason besides the death benefit. As I've always said, if you want a life long death benefit that gradually increases throughout your life, then a whole life insurance policy is a great way to get that (although a guaranteed universal life policy can provide a level life long death benefit at about half the price and is probably a better solution for those who really need a permanent death benefit). Bear in mind that you are likely to leave a larger inheritance by investing in stocks and real estate than buying life insurance due to the higher returns, and those assets, just like life insurance, provide a tax-free inheritance to your heirs. Life insurance only provides a larger inheritance if you die well before your life expectancy.

Myth #40 — You Get an Investment and Life Insurance

This one confuses a lot of people and they get really mad when they realize how whole life insurance works. They mistakenly believe that they get a death benefit for their heirs AND a separate “cash value” investment type account that they can use themselves or leave for their heirs. What they do not realize is these two pots of money are one and the same. That which you use for yourself does not get passed on to your heirs. When they discover this fact, they feel like the insurance company is stealing a bunch of money from them and their heirs.

In reality, when you borrow against your life insurance policy, you are borrowing against your death benefit. When you die, your heirs get the death benefit minus any outstanding loans. The amount of the outstanding loans, of course, can never be more than the cash surrender value of the policy, which gradually grows to an amount very close to the death benefit at your life expectancy. So really the cash value just tells you how much of the death benefit you can borrow at any time. You can either borrow this pot of money (death benefit/cash value/surrender value) and spend it yourself, surrender the policy and spend the money, die and leave the money to your heirs, or some combination of the above. But there isn't two pots of money. There isn't a $400K cash value and a $1M death benefit. There is just a $1M death benefit. If you spend $400K of it, your heirs only get $600K of it. So you don't get an investment AND life insurance, you get an investment OR life insurance.

Summing It Up

There you go. Forty reasons for buying whole life insurance debunked. Jangan khawatir; the agents who sell this stuff will come up with more. Just hang out in the comments section over the next year or two and you can watch. Whole life insurance is a product designed to be sold, not bought and the only way to win an argument with an agent trying to sell it to you is to stand up and walk away. As Upton Sinclair famously said, “It is difficult to get a man to understand something, when his salary depends on his not understanding it.” Maybe it should be called Whole LIE Insurance.

Whole life insurance is a terrible investment if you don't hold on to it to your death. Since the vast majority of people surrender their policies prior to death, it is a terrible investment for the vast majority of those who purchase it. If you want to invest in it, then you need to place a very high value on its unique aspects and not mind it's serious downsides.

The ideal purchaser of whole life insurance should:

- Need or desire a guaranteed, but possibly slowly increasing, life-long death benefit,

- Understand that the guarantee/contract essentially relies on the insurance company staying in business for as long as he lives for any policy of reasonable size,

- Live in a state that protects 100% of the cash value from creditors,

- Have some estate planning liquidity issues,

- Be in excellent health,

- Pursue no dangerous hobbies,

- Not mind having low returns on his investment despite holding it for decades,

- Have serious philosophical aversion to using traditional financing resources such as banks and credit unions (or simply just saving up for what you want to buy),

- Have already maxed out all available retirement accounts including backdoor Roth IRAs and HSAs, and

- Be willing to hold on to the policy until death no matter what changes in his financial life in the future.

The fact is that only a tiny percentage of the population, far smaller than the number of people who have been sold these policies historically, meets all or even most of these criteria. Whole life insurance remains a product designed to be sold, not bought.

Have more questions about life insurance and what kind of policies would be best for you? Hire a WCI-vetted professional to help you sort it out.

Agree? Disagree? Please reference which “myth” you're referring to in your comment and keep comments civil and on topic. Ad hominem attacks will be deleted.

[This updated post was originally published as a series from 2013-2019.]

The White Coat Investor may receive compensation from White Coat Insurance Services, LLC; licensed in all states including MA and DC; CA license #6009217; NY license #1758759 (exp. 6/2027); Registered address:10610 S. Jordan Gateway, #200 South Jordan, UT 84095. This does not affect the cost or coverage of insurance.

-

Apa itu Dogecoin dan bagaimana cara membelinya?

Dogecoin adalah sejenis cryptocurrency yang dimulai sebagai spoof pada Bitcoin — ya, lelucon! Sekarang ini adalah salah satu mata uang kripto yang paling bernilai tinggi, sebagian berkat plug dari CEO

-

Penabung Super Membuat Pengorbanan Ini untuk Meningkatkan Cadangan Tunai Mereka